Algunas deudas serán necesarias para pagar la educación de tus hijos o para generar nuevos ingresos

Seguramente, desde que eras pequeño has escuchado con insistencia que las deudas no eran buenas para tu salud financiera y que por lo tanto debías evitarlas. En parte tenían razón; no es muy inteligente que vivas eternamente endeudado con la tarjeta de crédito porque la utilizas para pagar tus gastos de consumo. Muchos padres también decían que solamente había que pedir prestado en momentos muy críticos, porque además de la vergüenza que eso causaba, quizás se tuvieran dificultades para honrar el compromiso de devolver el dinero recibido en las condiciones pactadas.

Es cierto que no todo lo que brilla es oro, pero tampoco todo lo que veas de color negro es carbón. Hay casos en que las deudas se adquieren para algo más noble que comprar el teléfono portátil de última generación, o para irnos un mes de vacaciones a una paradisíaca isla caribeña. A veces necesitarás endeudarte para la educación de tus hijos o para generar ingresos, por ejemplo: cuando compras herramientas y equipos que necesitas para hacer tu trabajo, o cuando te inscribes en un seminario de formación; ese tipo de deudas son necesarias y el hecho de que las adquieras demuestra que estás actuando de manera inteligente. También puedes endeudarte para comprar un bien del que sabes que aumentará su valor con el paso del tiempo. En cada uno estos casos, estarás adquiriendo una deuda buena porque gracias a ella, a la larga podrás mejorar tu situación financiera, tu bienestar y tu calidad de vida. Asume que la deuda buena es aquella que adquieres para comprar bienes que aumentan su valor con el paso del tiempo, o las que te permiten obtener beneficios económicos (inmediatos o futuros). Considera también que una deuda es buena cuando adquieres bienes que te permiten reducir los gastos recurrentes. Como verás, no es lo mismo pedir dinero prestado para el consumo inmediato (que no te reportará ningún beneficio económico) que endeudarte para asegurar la educación de tus hijos, o para hacer una inversión a medio o largo plazo.

De manera general, asume que la deuda mala (la que debes evitar) es la que contraes en función de tus hábitos de consumo. Si necesitas pagar el mercado semanal con tarjeta de crédito y te excedes en el plazo de pago sin intereses, estarás adquiriendo una deuda mala porque: 1) estás gastando lo que no tienes; 2) te estás endeudando para poder vivir, y 3) no solamente tendrás que devolver (tarde o temprano) el dinero que pediste prestado, sino que lo tendrás que hacer pagando los intereses (que no son bajos), con lo que tu probabilidad de ahorro será cada vez menor. Igual ocurre con los pagos con tarjeta de crédito en restaurantes (salvo que lo hagas para convencer a tu cliente y firmar un buen contrato), o los préstamos para equipar tu casa, salir de vacaciones, o para adquirir el vehículo, por citar algunos ejemplos.

Uno de los grandes errores que se cometen es caer en la tentación de comenzar a pagar un bien o servicio 3 o 4 meses después de adquirido e incluso luego de haberlo disfrutado. Imagínate que tengas la posibilidad de irte dos semanas de vacaciones a Tahití, sin pagar absolutamente nada hasta dentro de 3 meses. ¿tu que harías si dispusieras del tiempo para ello? ¿Durante cuántos meses o años verías mermada tu capacidad de ahorro por esas dos semanas de vacaciones?

Otro error muy grave es el de recurrir a una agencia de consolidación de deudas, o solicitar préstamos rápidos en efectivo (que los aprueban en cuestión de minutos). Por lo general, los clientes que acuden a estas empresas son personas que atraviesan una mala situación financiera y sienten un alivio momentáneo al contratar con ellas, sin considerar que no solamente se mantienen las razones de sus problemas financieros, sino que agravan la situación, puesto que ahora la deuda es mayor que la que tenían.

Dos recomendaciones finales: la primera, nunca te dejes seducir por el crédito fácil y la segunda, antes de endeudarte, pregúntate si verdaderamente necesitas lo que vas a adquirir, asegúrate de que vale la pena y de que estás en condiciones de pagar las cuotas mensuales y las anualidades (no creas que Dios proveerá); piensa en lo que debes sacrificar con la deuda que estás adquiriendo y en los posibles beneficios que esa decisión te reportará. Toma la decisión de endeudarte si después de responder estas preguntas, estás convencido de que tu mejor opción es el endeudamiento.

It is not necessary to have large fortunes to have the need to develop the family budget. Many families think that this budget is not necessary because they only have a modest source of income and their monthly expenses are typical of any average family, like paying rent, utility bills, some escapades to the movies, school for children, or vehicle expenses. Regardless of the economic slack your family may have, you need to prepare the family budget.

Just as it happens in a company, if you do not adequately handle the household economy, you’ll be committing serious mistakes with dire consequences for your pockets (and your health), and you’ll be repeating again and again the infamous phrase: “I can’t make ends meet“.

To avoid such awkward moments, you must bring order to your domestic economy and the first practical step to achieve this is to develop a simple family budget. The budget will bring the bills on time and help you avoid wasting money, allows monitoring of costs to reduce them, prioritize or delete them as far as possible; In addition, if you meet the budget by knowing the economic situation of your family to date, you will be able to make better forecasts, inviting the savings and to protect yourself against unforeseen events such as illness, damage to housing, vehicle breakdowns, etc.

A basic budget has two columns: the INCOME column and the EXPENSES column. In the income column you’ll write any money entries that sustain your family: wages, overtime, financial aid and generally any other source of income your family has during the month.

In the expenses column, you will record all monthly expenses classifying them into three categories:

- Compulsory expenditure (which you can not stop paying and they are constant); for example, rent or home mortgage, a bank loan that you have requested, quotas for Social Security, or payment of your community.

- Necessary expenses (you can not stop paying them, but you can reduce the amount of what you pay); Typical examples of this category correspond to electricity bills, water, telephone, expenses for food, clothing, transportation, etc. You see, you can not help incurring such expenses, but you can take steps to reduce the amount you pay.

- Occasional expenses that can be totally eliminated if necessary, for example leisure and recreation expenses (food and beverages away from home, horseback weekend), non essential consumer goods, electronic equipment, etc.

Once you have registered with honesty all income and all expenses, summarize both columns and get the difference between the two. If the column total expenditure is greater than total income, then I don’t need to tell you (because you’ll already have noticed) that you are in serious economic problems and should start as soon as possible to eliminate incidental expenses and reduce the amount of necessary expenses (unless you’re able to earn more income). If, however, the income column is greater than expenses, you must interpret this difference as your ability to save; if so, mark the aim of saving at least 10% of your monthly income and commit to it.

Remember that the goal is to make the family budget income to cover your family living costs; so when you establish the budget, involve the family for a global commitment to savings and avoiding wastage. The budget will help you identify and eliminate unnecessary costs, reduce unnecessary expenses and reduce bills for necessary expenses.

To have more slack and for your budget to be your best financial partner, avoid as far as possible the use of credit cards, and beware of getting into long-term debt or high interest rates credits as possible (especially consumer credits or loans) and most importantly, never ever forget the golden rule: do not spend beyond your means.

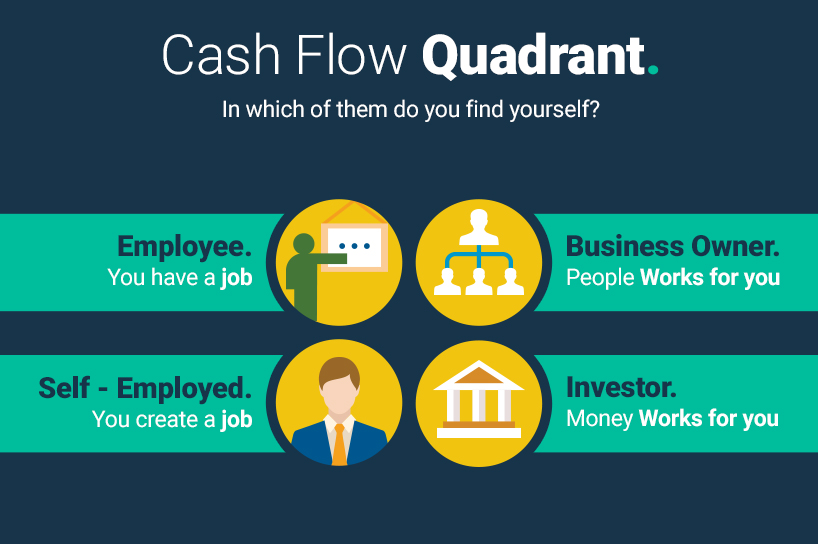

One of the most used diagrams to understand who we are and how we think is the famous money flow quadrant, designed by Robert Kiyosaki to chart the four profiles of people, according to the manner in which they mainly derive their income.

Each quadrant has its own particularities. The way you earn money will depend in which quadrant you are, which –in turn- will depend on the way you think, your interests, your educational background and your skills.

The chart is divided into four quadrants (E-S-B-I)

People located in quadrant [E] (EMPLOYEE) are those who want job security, with a good pay and benefits to offset all the time they devote to meet the financial goals of others. In this quadrant, it doesn’t matter if you’re a delivery guy or an executive officer; In both cases, the money earned is the product of a contractual relationship; That’s what matters. From a financial standpoint, this group of people depends entirely on a salary and other compensations paid by their employers. In short, people on quadrant [E] are employed.

People on quadrant [S] (SELF EMPLOYED) also want security in their financial income, but unlike employees they don’t work for others in a fixed salary, but by maintaining autonomy and control over themselves as well as the work they do and the financial compensation they expect to acquire in terms of knowledge, experience, work hours and the quality of the work they try to do. People in this quadrant focus on the product and have been proven reluctant to delegate. This group is characterized by the abundance of well-trained professionals in specific areas who work on their own (doctors, architects, painters, masons, gardeners, mechanics, dentists, commissioned salespeople, consultants, etc.). In addition to financial appreciating safety, people in this quadrant also value freedom and autonomy. In short, people on quadrant [S] are in control and own their own employment.

The third quadrant [B] (BUSINESS OWNER) corresponds to people whose profiles are opposite to that of employees. They like to delegate and expect others to be the ones who do the work that will benefit them financially. People in this quadrant have the property or have control over the business system; They strive to make the best of the people who surround them and show skills to lead people.

Unlike people from quadrant [S] who focus on the product and whose profit depends on their direct work, people who are in quadrant [B] focus on a comprehensive business system, so they don’t have the need for direct jobs for their income; thus ensuring that money keeps on entering their bank accounts, even when they’re on vacations or physically indisposed to perform some work. In short, people on quadrant [B] have a business system and hire people who will make them earn money thanks to their work.

Finally, the fourth quadrant [I] (INVESTORS) corresponds to those that focus on making money without working, making money work for them. They are people who know and are able to take risks. According to Kiyosaki, in this quadrant is where the money becomes wealth when considering that it is not measured in currency units (or money) but in the number of days that you can live without working directly and maintaining (or even increasing) your welfare and quality of life. In short, people within the quadrant [I] do not need to work directly, or hire people to do the work. Is the money that works for them.

After this quick walk through the money flow quadrant:

- In which of them do you find yourself?

- Have you decided to cross the borders of the quadrant in which you find yourself today?

- In which quadrant you want to be within 3 or 5 years?

- What are the first steps you will take to achieve it?

Finding the answers to these questions will help you make good decisions that will improve your quality of life and bring you closer to achieving your financial goals.

Your Financial Net Worth is one of the indicators that illustrate the ability to achieve financial goals for the short, medium or long term. Basically, it is the result of subtracting your liabilities worth from your assets valuation; that is to say:

Financial Net Worth = Financial Assets – Financial Liabilities

First things first:

To calculate your total Financial Assets, you must know that the most important thing to keep in mind is that your assets correspond to the physical cash you possess to purchase things either now or later. You can also consider as financial assets, those investments that can be converted into fiat money. Consumer goods, such as your clothes, TV, washing machine, furniture and fixtures (unless you’re thinking of selling them) should not be considered as financial assets because they do not contribute to putting money in your pocket.

On the other hand, generally, Financial Liabilities include all debts that you have and any other payment commitment or contractual obligation you have acquired and that involves paying in cash or handing over a financial asset. There are short and long term liabilities, enforceable and unenforceable, contingent liabilities and other, but we’ll leave that for later. For now, the important thing is that you recognize the fundamental differences between assets and financial liabilities.

A simple way to understand the difference between assets and liabilities, is assuming that an asset is anything that puts money in your pocket and a liability is anything that takes it away from you.

Each person, depending on their circumstances, interests and goals, will interpret in one way or another the value obtained by subtracting liabilities from assets; but in any case, a very good recommendation is that you calculate your Financial Net Worth now. Know how much money you have, how much you owe and how much you have left, and then act trying to eliminate the debts of major importance so that once you’ve cleaned up your finances, you begin to build a financial base that allows you to live comfortably (without strain) for at least three months.

Thus, without realizing it, you’ll be starting to get your financial freedom and you may regret not having done so before.

Financial intelligence incorporates multiple dimensions and transcends the mastery of the concepts of finance.

Robert Kiyosaki says: “Financial intelligence refers not so much to how much money you earn, but how much money can you keep, how hard that money works for you and for how many generations it has been preserved.” Obviously, obtaining financial independence by constructing a business system (quadrant D) or by investing (quadrant I) requires that we have a degree of intelligence applied to the world of finance.

But financial intelligence is not only essential for those who live on the right side of the Cash Flow Quadrant; it is also needed by those at the left side: those who are not comfortable in their role of employees (quadrant E) or who independently and on their own work long hours to ensure economic sustainability (quadrant A). With certain knowledge and enough willingness to break emotional attachments, these people can begin to design a system of self-generating money and thus cross the threshold of their respective quadrants.

Obviously, financial intelligence is not limited to the mastery of the concepts of finance, but also is associated with leadership, strategic thinking, personal marketing, communication, negotiation, conflict management, social skills and management of emotional heritage, and others.

A good way to identify to what extent you possess financial intelligence, is checking the following items:

- Your income is greater than your expenses (you have capacity for saving).

- You manage to find new forms of income (in several quadrants simultaneously).

- You have identified your financial goals and you have designed your task list to achieve them.

- You know how to optimize and earn higher returns on capital.

- You feel you are on the right track to achieve your financial freedom.

The people possessing a meaningful financial intelligence always think big, and regardless of the circumstances surrounding them, continually design plans to enhance their assets and reduce their liabilities, thereby obtaining greater profitability and liquidity while they improve their quality of life.

If you want to have a financial culture that is your ally in the life project you’ve designed, you must start by understanding the functioning of money as well as the psychological aspects that drive people to use it in a certain way.

The key you need to gain and retain money is just a good financial education that contributes with the foundations needed for you to think and act.

Everyone wants to make money (some more than others), but if you really want to make money in the best way possible and for longer, the worst decision you can make will be to go out right now and try to find a good job hoping to stay a long time on it, because even if you find it, you will never have the certainty of getting the money you really want, and worse, if you get it, you may be unable to keep it, and then you will always depend on others. Remember that lifetime wages are long gone.

Keep in mind that it is not just to make money. The fact that you earn a lot of money today is no guarantee that you’ll have it tomorrow. What this really is about is that you retain that money, and your children and grandchildren should also benefit financially from what you’re doing today. So no matter how much money you make; the important thing is how much money you are able to keep, and for that there is no magic formulas or recipes.

The most important thing that you really need in order to earn and retain money is a financial education that will contribute to a good foundation for thinking and acting from the conviction that you are never going to achieve economic independence by having a good job nor even working on your own, literally forcing you to crush yourself hour by hour to more or less satisfy your basic needs and indulge yourself with an occasional treat. Always keep in mind that you deserve more than that.

Do you think you’re a person prepared to win and keep money? See if it’s true; try to answer this question as honestly as you can: Do you really know the difference between an asset and a liability? If your financial knowledge is what most people has, maybe you’re acquiring liabilities believing they are assets; and the worst is that without realizing it you’re building your own financial problems.

From a practical perspective, the first and most important rule to make money and keep it is to acquire assets, because as Robert Kiyosaki (author of Rich Dad Poor Dad) says, assets are those that put money in your pocket while liabilities will extract it (sometimes without you even realizing it). The difference between your assets and liabilities is your Net Worth. Until you assume this basic principle, you will find yourself with serious difficulties in making judgments and taking the best financial decisions on how to earn and keep your money.

Above all, remember that your time, your knowledge and skills are very valuable to only be exploited by others. Avoid selling your time in exchange for money; Use it rather to learn, design, build and implement a system that is able to generate money for itself.

The more widespread and positive your Net Cash Flow is, the greater the leeway to deal with unexpected expenses will be.

One of the most basic terms of personal finance is the one known as the Net Cash Flow, so much so that your personal or family financial situation can be easily diagnosed by a quick glance at it.

The Net Cash Flow describes the revenues and expenditures of cash during a determined period of time (for example, a month or a year). If you spend less than you earn, your cash flow will be positive and will increase your net worth; on the other hand, if your expenses are greater than your income, your cash flow will be negative and you will be wasting your net worth, which is not sustainable over time and requires that you take a prompt decision.

The more positive and larger your cash flow is, the greater the leeway you will have to deal with unforeseen contingencies, as well as it contributing to obtaining the financial independence you want. Your peace of mind, freedom and quality of life will improve substantially.

To increase your cash flow, you don’t necessarily have to earn more money; you can increase it by reducing the amount of your recurring expenses (for example, the monthly utility bills), or decreasing unnecessary expenses (for example, buying the latest mobile phone or buying a bigger TV). Another way (maybe the fastest) is to reduce your debts (like Credit Cards or the loan for the purchase of your car).

In any case, always remember that what you are looking for with your financial decisions is to improve your quality of life and to progressively get closer to your goals. Maintaining your Net Cash Flow under control will help you achieve it.

If you want to start playing at the world stock market, the “blue chips” could be a good investment option

No wonder that a significant number of investors prefer to operate with the so called Blue Chips. This tems, which referes to casino blue chips (which are those that represent more value) is used in the stock exchange world to identify stocks of stable companies, financially solid, well-established and with products or services with good acceptance. Typically, blue chips correspond to the stocks of financial institutions globally recognized, as well as the leader multinationals in sectors like energy and telecommunications.

The shares of these businesses are very attractive to investors for their reliability, the evolution of the price is uniform, remaining stable to market swings; Blue chips can be traded when desired and, sometimes, payment of dividends (shareholder earnings) is done on a regular basis even though the company is not going through its best moment.

A good way to understand the blue chips is considering them as the premium stocks in the market: stable, with predictable yield (although lower than others) and with little financial risk, making them ideal for conservative investors, cautious and with little tolerance for uncertainty and risk.

As is to be expected in any investment, profitability is proportional to the risk; in the case of the blue chips, profitability is fairly low and due to high demand, these stocks tend to have higher prices, so they are not attractive for those who want quick profits; however, they are a good way to start playing on the market.

Had you ever thought about being a shareholder of a large bank? By buying blue chips, you are not only taking your first steps into the world of investments and getting dividends from time to time, but also, you will be owner of a small part of that business; a very small part, but that is the starting point.

Always try to get the money you need doing what you really love

When you have the ability to satisfy all your financial needs, without relying on anyone nor doing something that you do not like, you may say that you enjoy an economic wellbeing and that you have financial freedom.

The opposite of financial freedom is the financial dependence, this is when people are dependent on others to provide them the money they need to cover the expenses for their needs and support their lives.

MONEY RACE STUDIOS 2020 - ALL RIGHTS RESERVED - LEGAL NOTICE - PRIVACY POLICY