It is not necessary to have large fortunes to have the need to develop the family budget. Many families think that this budget is not necessary because they only have a modest source of income and their monthly expenses are typical of any average family, like paying rent, utility bills, some escapades to the movies, school for children, or vehicle expenses. Regardless of the economic slack your family may have, you need to prepare the family budget.

Just as it happens in a company, if you do not adequately handle the household economy, you’ll be committing serious mistakes with dire consequences for your pockets (and your health), and you’ll be repeating again and again the infamous phrase: “I can’t make ends meet“.

To avoid such awkward moments, you must bring order to your domestic economy and the first practical step to achieve this is to develop a simple family budget. The budget will bring the bills on time and help you avoid wasting money, allows monitoring of costs to reduce them, prioritize or delete them as far as possible; In addition, if you meet the budget by knowing the economic situation of your family to date, you will be able to make better forecasts, inviting the savings and to protect yourself against unforeseen events such as illness, damage to housing, vehicle breakdowns, etc.

A basic budget has two columns: the INCOME column and the EXPENSES column. In the income column you’ll write any money entries that sustain your family: wages, overtime, financial aid and generally any other source of income your family has during the month.

In the expenses column, you will record all monthly expenses classifying them into three categories:

- Compulsory expenditure (which you can not stop paying and they are constant); for example, rent or home mortgage, a bank loan that you have requested, quotas for Social Security, or payment of your community.

- Necessary expenses (you can not stop paying them, but you can reduce the amount of what you pay); Typical examples of this category correspond to electricity bills, water, telephone, expenses for food, clothing, transportation, etc. You see, you can not help incurring such expenses, but you can take steps to reduce the amount you pay.

- Occasional expenses that can be totally eliminated if necessary, for example leisure and recreation expenses (food and beverages away from home, horseback weekend), non essential consumer goods, electronic equipment, etc.

Once you have registered with honesty all income and all expenses, summarize both columns and get the difference between the two. If the column total expenditure is greater than total income, then I don’t need to tell you (because you’ll already have noticed) that you are in serious economic problems and should start as soon as possible to eliminate incidental expenses and reduce the amount of necessary expenses (unless you’re able to earn more income). If, however, the income column is greater than expenses, you must interpret this difference as your ability to save; if so, mark the aim of saving at least 10% of your monthly income and commit to it.

Remember that the goal is to make the family budget income to cover your family living costs; so when you establish the budget, involve the family for a global commitment to savings and avoiding wastage. The budget will help you identify and eliminate unnecessary costs, reduce unnecessary expenses and reduce bills for necessary expenses.

To have more slack and for your budget to be your best financial partner, avoid as far as possible the use of credit cards, and beware of getting into long-term debt or high interest rates credits as possible (especially consumer credits or loans) and most importantly, never ever forget the golden rule: do not spend beyond your means.

He who has never been afraid of losing money can cast the first stone?. It’s obvious that nobody likes losing money; we care for it as if it were our most precious asset, but we should understand on how that fear can affect our attitude.

The fear of losing money is inevitable (for both poor and rich folks); It is not a fear of cowards, but a necessary fear. The bottom line is not about fear itself, what’s really interesting is how that fear affects us emotionally; in other words, how we manage our money in spite of that fear. On occasions, people fear so much the possibility of losing money, they won’t take any kind of risks, instead they will play it safe and end up losing.

How to manage the perception of fear, the sensation of lost and the experience of failure?

One of the best tricks to overcome your fear of losing, is redefining the concept of failure. What is the meaning of failure for you? You can see it as a tragedy or as a learning experience; You can understand it as a sign to let your plans succeed, or you can view it as an inspiration to go even beyond your desires. Possibly you see failure as a punishment for your ambition, or perhaps you prefer to understand it as a new opportunity; You can also see it as a defeat, while others see it as a sign to start over but more experienced.

Some people get weakened in face of failure, while others grow stronger. How and why does this happen? Basically, the difference won’t be found on objective matters, such as academic degrees, where they live, their age, or their wealth. The difference between one way of seeing the consequences of failure and the other lays on the attitude, and your attitude depends on what you believe in.

Concretely speaking, the fear of losing money is rooted in the fear of failure, and one of the practical ways recommended to overcome the fear of losing money is to assume that no one will take it out of your hands (unless you let them); money also won’t disappear by itself (unless you throw it out the window and the wind carries it away). In any case, you are the great money manager and you know there is no success without taking risks and learning. The more you acquire skills to manage your money, the less aversion to failure you’ll have, and therefore you’ll have less concerns at the possibility of losing money. Remember that no one has become rich without losing some money.

At this point it is well worth extracting a powerful phrase from the book “Rich Dad Poor Dad” whose author, Robert Kiyosaki, says bluntly that the losers avoid failure, while failure turns losers into winners. So you shouldn’t panic in the face of failure because your natural response to that fear will be to do nothing, and you shouldn’t stop playing in fear of losing. Also don’t get compliant for playing it safe because, even when winning, you would not have learned much. Do not forget that you have the sufficient capacity to win, and if you end up losing money, do not worry because you will always have the tools and skills to find new opportunities to recover and recapitalize.

Our final recommendation: don’t be afraid of losing money and never think in terms of poverty, because that is always followed by a large army of burdens, fears and apprehensions.

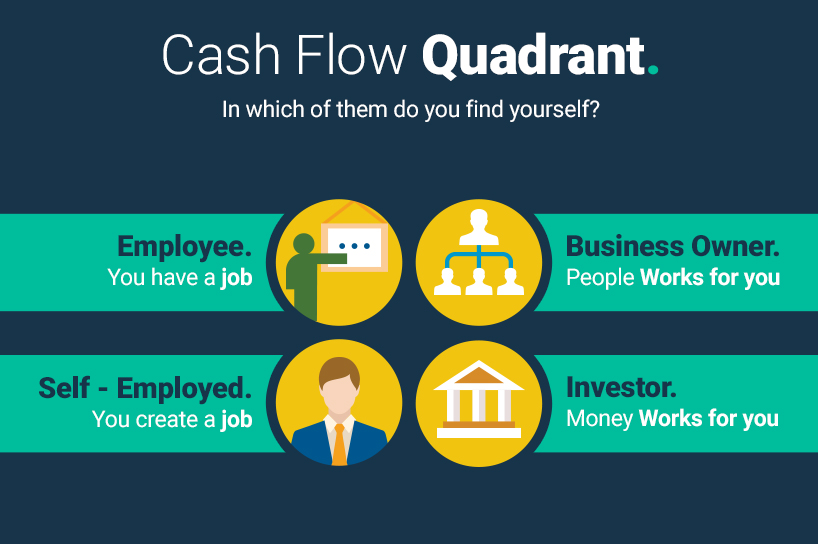

One of the most used diagrams to understand who we are and how we think is the famous money flow quadrant, designed by Robert Kiyosaki to chart the four profiles of people, according to the manner in which they mainly derive their income.

Each quadrant has its own particularities. The way you earn money will depend in which quadrant you are, which –in turn- will depend on the way you think, your interests, your educational background and your skills.

The chart is divided into four quadrants (E-S-B-I)

People located in quadrant [E] (EMPLOYEE) are those who want job security, with a good pay and benefits to offset all the time they devote to meet the financial goals of others. In this quadrant, it doesn’t matter if you’re a delivery guy or an executive officer; In both cases, the money earned is the product of a contractual relationship; That’s what matters. From a financial standpoint, this group of people depends entirely on a salary and other compensations paid by their employers. In short, people on quadrant [E] are employed.

People on quadrant [S] (SELF EMPLOYED) also want security in their financial income, but unlike employees they don’t work for others in a fixed salary, but by maintaining autonomy and control over themselves as well as the work they do and the financial compensation they expect to acquire in terms of knowledge, experience, work hours and the quality of the work they try to do. People in this quadrant focus on the product and have been proven reluctant to delegate. This group is characterized by the abundance of well-trained professionals in specific areas who work on their own (doctors, architects, painters, masons, gardeners, mechanics, dentists, commissioned salespeople, consultants, etc.). In addition to financial appreciating safety, people in this quadrant also value freedom and autonomy. In short, people on quadrant [S] are in control and own their own employment.

The third quadrant [B] (BUSINESS OWNER) corresponds to people whose profiles are opposite to that of employees. They like to delegate and expect others to be the ones who do the work that will benefit them financially. People in this quadrant have the property or have control over the business system; They strive to make the best of the people who surround them and show skills to lead people.

Unlike people from quadrant [S] who focus on the product and whose profit depends on their direct work, people who are in quadrant [B] focus on a comprehensive business system, so they don’t have the need for direct jobs for their income; thus ensuring that money keeps on entering their bank accounts, even when they’re on vacations or physically indisposed to perform some work. In short, people on quadrant [B] have a business system and hire people who will make them earn money thanks to their work.

Finally, the fourth quadrant [I] (INVESTORS) corresponds to those that focus on making money without working, making money work for them. They are people who know and are able to take risks. According to Kiyosaki, in this quadrant is where the money becomes wealth when considering that it is not measured in currency units (or money) but in the number of days that you can live without working directly and maintaining (or even increasing) your welfare and quality of life. In short, people within the quadrant [I] do not need to work directly, or hire people to do the work. Is the money that works for them.

After this quick walk through the money flow quadrant:

- In which of them do you find yourself?

- Have you decided to cross the borders of the quadrant in which you find yourself today?

- In which quadrant you want to be within 3 or 5 years?

- What are the first steps you will take to achieve it?

Finding the answers to these questions will help you make good decisions that will improve your quality of life and bring you closer to achieving your financial goals.

Your Financial Net Worth is one of the indicators that illustrate the ability to achieve financial goals for the short, medium or long term. Basically, it is the result of subtracting your liabilities worth from your assets valuation; that is to say:

Financial Net Worth = Financial Assets – Financial Liabilities

First things first:

To calculate your total Financial Assets, you must know that the most important thing to keep in mind is that your assets correspond to the physical cash you possess to purchase things either now or later. You can also consider as financial assets, those investments that can be converted into fiat money. Consumer goods, such as your clothes, TV, washing machine, furniture and fixtures (unless you’re thinking of selling them) should not be considered as financial assets because they do not contribute to putting money in your pocket.

On the other hand, generally, Financial Liabilities include all debts that you have and any other payment commitment or contractual obligation you have acquired and that involves paying in cash or handing over a financial asset. There are short and long term liabilities, enforceable and unenforceable, contingent liabilities and other, but we’ll leave that for later. For now, the important thing is that you recognize the fundamental differences between assets and financial liabilities.

A simple way to understand the difference between assets and liabilities, is assuming that an asset is anything that puts money in your pocket and a liability is anything that takes it away from you.

Each person, depending on their circumstances, interests and goals, will interpret in one way or another the value obtained by subtracting liabilities from assets; but in any case, a very good recommendation is that you calculate your Financial Net Worth now. Know how much money you have, how much you owe and how much you have left, and then act trying to eliminate the debts of major importance so that once you’ve cleaned up your finances, you begin to build a financial base that allows you to live comfortably (without strain) for at least three months.

Thus, without realizing it, you’ll be starting to get your financial freedom and you may regret not having done so before.

If you do not have credit history, or if you ever have been denied credit, it’s time you start thinking about a secured credit card. As you know, the way you use credit cards widely impacts your financial history; so to make a good start on that history, or to restore a situation of a somewhat weak credit, a good option is to use this type of financial instrument.

In those cards, credit is secured by a deposit made in a saving account specially designed for this purpose. Thus, the credit limit will depend on the amount of that deposit.

Lots of people confuse secured credit cards with prepaid debit cards (or just prepaid cards). These work just as a normal debit card, with the proviso that the available funds have been previously pre-loaded. This category includes discount cards and the ever popular gift card.

With the intention of helping to create responsible spending habits and to contribute with security by taking away the necessity of paying with cash, many parents choose to give prepaid cards to their children; but nevertheless, and contrary to what happens with secured credit cards, the emission of the prepaid card in not informed to the credit agency, and thus the way it’s used won’t have any effect on the construction and consolidation of their personal credit history.

Although in both cases funds are guaranteed, it’s preferable to operate with the secured credit cards, since besides establishing and managing your own credit limit, you’ll be able to build a solid financial history, then within two months, the bank entities could provide the opportunity to apply for a new credit card without the down payment.

There are people decided to enter the business world, but without the necessary experience to commercially exploit certain product or service. For them, acquiring the rights to use a trademark, along with experience and key knowledge, is without doubt an attractive business formula and a very good investment option, but sometimes you can get unpleasantly surprised.

Fairs and franchising exhibitions are becoming increasingly frequent, and they are already part of the usual agenda of each year. As you know, this fairs are attended by the owners and representatives with a clear desire to sell, and therefore strive to project an image of reliability and solidity.

Trying to show the best image possible has always been important in all areas in which human beings are involved, but here is at stake both your money and your financial future; therefore, when evaluating a franchise, the first thing to avoid is to get yourself caught by the attractiveness of a franchise stand, the utilities and items offered, or multicolored well-designed commercial brochures.

Since not all franchises are equal and to avoid exposing your money and taking unnecessary risks, you should look to invest in a franchise for which you can assess how attractive it is and how much its strength is. One of the first signs that you receive from a reliable franchise, is that when you show interest in it, their representatives strive to make you understand the history of the franchise along with all its business information, putting financial data at your disposal as well as growth and expansion plans. This would be a good way to get the confidence you need to further evaluate other options. Transparency is the fundamental base of business; so you must demand it in matters that really are of your interest. In the opposite case, unreliable franchises do not try to convince you about the attractiveness of the business, instead they are trying to make an immediate sell, offering “great advantages” if you sign the contract right away.

Once you overcome that first and very important contact, common sense dictates that if you are interested in a particular brand the second step is to know certain details that will provide you greater certainty and reliability; for example: how strong is the brand you want to market in your geographic market space? What do other people who share the sector of activity in which you want to dabble in think about that brand? It’s also important that you inquire about the innovation policies that have launched the franchise and what benefits you will get from such policies. This question should also be asked about the technical and commercial assistance and in relation to product development.

Of course, it’s not enough to know the appeal of the brand to make the decision, do you already you have information on the loan and the conditions required by your creditor bank? Have you analyzed the performance figures? How long before the business will start giving profits? Can you afford that time? If the franchise gives you part of the financial support you need, in what terms would be agreed such conditions?

Finally, before getting any obligation or contractual commitment, and even if you are convinced of the attractiveness in terms of technical, financial and commercial aspects, it is advisable to seek advice from a lawyer with experience in the world of franchising. The legal advice will not only protect you against possible cases that may arise, but also will advise you on proper financial aspects, including of course the tax and labor issues you cannot ignore. As you can see, there is no way to separate franchises from finances; both go hand in hand, and while it is true that franchises aimed at the fashion industry and fast foods are the most demanded, do not forget to evaluate other options in non-traditional sectors, since the investment will be substantially lower and return rates are quite significant.

When you’re going to invest, the first questions you need to ask yourself is: Is it a worthy investment? Is it advisable to take the risk? One of the most important evaluations to differentiate one investment alternative from another is the combination of risk that you will assume, and the benefits you expect to get (profitability).

Generally, rikier investment should produce higher returns. If it were not so, any investment alternative that report the same potential benefits to another with a lower risk would cease to be attractive.

The risk is linked to the uncertainty of the benefits you actually get by investing. You can earn more than what you expect, less than desired, or you can even lose all the money you invested. There is no way to avoid the risk because profitability will never be assured.

Each alternative for investment is unique because it combines risk with profitability. Since not all alternatives have the same risk or the same return, there are two “laws” that common sense dictates and you should consider when choosing:

- Between two alternatives with EQUAL RISK, you must choose the MOST PROFITABLE ONE.

- Between two alternatives with equal PROFITABILITY, you must choose the one with the LOWEST RISK.

As you can see, you cannot separate the risk that you will assume from the profitability you expect to get, and although an investment with greater risk should produce higher returns, be careful when deciding because there is no guarantee that that will happen. To accept a higher risk does not always lead to greater profitability.

Even though it seems strange, a good salary doesn’t guarantee financial success; also having a low salary does not mean failure. Financial success depends on how you manage your personal finances to improve your quality of life and achieve your goals, regardless of how much money you earn or how big is your spending budget.

Managing your personal finances is a process that begins with knowing your current financial situation; the process continues with the establishment and prioritizing of your goals, so that you can then develop certain strategies that will allow you to get going from your current situation to achieving your goals.

As you see, this is a comprehensive planning process. It is your quality of life that you’ll get to improve and for that you can’t just be focused on a particular interest, neglecting or leaving aside others. Proper personal financial planning will allow you to make smart decisions, including the purchase of your first home, emergency fund management, education for your children, or even how to secure your quality of life after retirement.

It’s not the one who earns the most money that lives better. The one who lives better is the one who is able to get the best possible quality of life, and personal financial planning acts like the map that marks the path to achieve your dreams, realise your ideals and reach your goals. Personal financial planning thus becomes an essential piece of your route; it helps you to achieve your dreams, prioritizes your goals, alerts you about the obstacles which you may find along the way, prevents you from making terrible mistakes, prepares you to face contingencies and unforeseen events and, last but not least, offers first class information so you can make the best decisions.

As you may have noticed, your financial success depends less on your income, but rather on the clarity of your goals and the route you have designed to manage your personal finances.

On many occasions you’ve probably felt like money controls your life. Perhaps you wanted to go for the weekend to the countryside or to the beach, but you could not because you had no money; possibly you needed to pay the electricity bill, but you had to leave it for the next month because you just barely had the money needed for groceries; your vehicle broke down, but you could not fix it because you had to deal with other priorities; In addition, your credit card was about to burst and you didn’t even pay the minimum quota in hopes that the bank would not notice that default in payment.

Surely, these miserable experiences made you feel bad; your mood and your self-esteem were markedly reduced, you got locked in your money problems, you lost your friends, and your thoughts just invited you to believe that it was all “because of money.”

Money is not responsible for our mood or our daily practices. Fortunately, we alone are responsible for our life and our future. A healthy way to change our perception of money is trying to answer these questions: How do I feel about money? What are my beliefs and expectations about money? Am I able to control my expenses and my savings? Is money the one that is controlling my life, or is it me who should control the money?

Your beliefs, perceptions and expectations affect your emotions and determine the actions you can take to sort your finances and expand your financial slack. I give you an example: as long as you don’t believe that you can be successful in life, you will think that there is no need to succeed in finances, so neither you will be convinced about the need to raise your income or moderate your expenses and, consequently, you won’t have reason to change your patterns of consumption, savings habits or your ideas on investment.

Another example: if you believe you’ll never have enough money to do what you please and live as you dreamed, you will unconsciously deny the control you have over your future (which nobody else but you has) and therefore you will not have aspirations, you won’t feel the need to take on challenges and design your financial road map; you’ll just feel resigned.

The concepts you have about yourself and money significantly influence your attitude and the actions you undertake to achieve your goals. Remember that the only person who controls what you think and feel is you. If you just repeat the phrase: “I have no money” I assure you that you will not be doing yourself any favors; On the contrary, you are reinforcing your negativity and slowly you will drag yourself down emotionally. Similarly, if your favorite phrase is: “my salary is not enough at all”, you will be reinforcing the idea that you are not responsible for what happens to you, but that the fault of your ills belongs to your salary, the employer who pays your salary, the government, or the bank.

Always keep in mind that your personal or familiar experiences with money have an influence on your beliefs and the expressions you use on a regular basis when you refer to it; also, those beliefs influence your values, your attitude and your spending, savings and investment habits; in other words, they affect how you manage your money.

Financial ignorance or poor money management can also cause you mental exhaustion, stress, low self-esteem, and even a decrease in the affection and the quality of our relationships with family and friends. Stay focused on your projects and improve your relationship with money; remember that this relationship affects you personally but also affects your relationship with other people.

Lastly, learn to control your feelings about money. Get rid of negative thoughts like “I’ll be poor all my life”, “I don’t know how to earn more money” or “I can’t do more than what I’m already doing.” Do not forget that you’re the only person able to control your future.

So now you know, control your feelings so that money does not control you.

It is very likely that the biggest and most important purchase we make in life is that of our first home. Upon signing our first mortgage we get excited and celebrate such an event without really considering the financial obligation we are contracting that we must honor for many years.

At first, there is no better feeling than having the keys to our own home; with the passage of time, that feeling fades and is replaced by the desire to get rid of debts; which is not unreasonable, because the simple fact of reducing expenses due to interest is already a way of saving; plus you will feel emotionally safe, you won’t owe anything to the bank and you’ll be able to say that the house is completely yours. That security is one of the biggest advantages of paying the mortgage early, even though you may have to assume certain expenses for anticipated pay off.

Perhaps you feel a wild urge to free yourself of your mortgage as soon as possible, but before doing so it is appropriate that before you try to pay off the debts with highest interest rates (eg credit cards or consumer loans), you build an emergency fund (at least it should meet expenses for 3 months of your lifestyle), and review your retirement plan.

If you decide to pay off your mortgage early, there are some recommendations:

- Make payments every two weeks. This may be the easiest way to shorten the lifespan of your mortgage. If you pay the minimal monthly quota every two weeks, you can reduce your mortgage commitment for approximately four years. It’s important to note that the payment is every two weeks, so if a year has 52 weeks, you will make 26 payments (equivalent to 13 monthly installments). This system allows you to bring forward the payment schedule and further reduce interest expenses, as the last two payments (25 and 26) will be applied to reduce the loan’s principal.

- Increase the monthly payments. Perhaps it is the most attractive method for users who have some capacity for saving. If you have a financial slack that allows you to pay an extra above the contractual obligation you got when you purchased your home, you will not only pay less interest, but also reduce the lifetime of the mortgage. It’s all about getting a pencil and doing the math.

- Making annual payments. Quite possibly, at the end of each year you enjoy a good economic situation because you receive bonuses, payments for utilities, compensation, additional wages or other extraordinary income; well, with some financial discipline you can use some of that surplus to repay the mortgage loan. As in the above cases not only you will pay off the mortgage early and get rid of that financial burden, but it also will reduce the interest expenses, which in a nutshell is a saving. Other people prefer to set aside a portion of the monthly surplus to later destine it to repay the loan through an annual payment; thus they ensure flexibility amid the financial discipline and maintain a fund to cover unforeseen situations or any contingency that may arise along that

- Refinancing the mortgage debt and reinvesting. If you don’t feel attracted to any of the above methods, you still have this option to reduce the lifetime of your mortgage. Current interest rates (rather low) are an incentive to refinance debt, and if you’re smart about it, it can also allow yourself to cancel your mortgage early. Obviously, you have to assess the cost of refinancing with your creditor Bank (because refinancing costs money) but if the new loan has favorable terms for you, you will probably have a greater saving capacity, which in turn you can reinvest and make advance payments applied to the loan’s principal.

In any case, the method you choose to free yourself from your mortgage early will depend on what makes sense to you. You must choose the option that you feel more comfortable according to your financial situation and your personal and family preferences.

MONEY RACE STUDIOS 2020 - ALL RIGHTS RESERVED - LEGAL NOTICE - PRIVACY POLICY